You are here

Diplomacy & Defense Think Tank News

Folgen der stockenden Verhandlungen zum globalen Anpassungsziel für Entwicklungsländer

Bonn, 6. Juli 2026. Gemeinschaften in besonders stark vom Klimawandel betroffenen Ländern passen sich an dessen Auswirkungen an, doch die nötigen Ressourcen bleiben aus.

Die alljährlichen Zwischenverhandlungen der UN-Klimarahmenkonvention im Juni (SB64) erreichten bei mehreren zentralen Agendapunkten, darunter dem Globalen Anpassungsziel (Global Goal on Adaptation, GGA), nur begrenzte Fortschritte. Das GGA ist eine Verpflichtung aller Unterzeichnerländer des Pariser Abkommens. Es soll die Anpassungsbemühungen koordinieren, Rechenschaftspflichten stärken und Finanzmittel für vulnerable Länder mobilisieren. Obwohl die Staaten den Umsetzungsrahmen finalisieren sollten, bleiben langjährige politische Streitfragen ungelöst. Entwicklungsländer kritisierten die Industrieländer, weil die schriftliche Einigung auf mindestens eine Verdreifachung der Anpassungsfinanzierung ausblieb, wie sie im „Mutirão“ der COP30 verankert ist. Ohne diese Einigung zur Finanzierung stocken die Verhandlungen.

Die festgefahrene Situation reicht über die Verhandlungsräume in Bonn hinaus. Für klimavulnerable Länder wächst mit der Lücke der Anpassungsfinanzierung die Kluft zwischen Klimaverpflichtungen und ihrer Umsetzung. Oft reichen nationale Anpassungsbudgets nicht aus und konkurrieren mit anderen dringlichen Entwicklungsprioritäten. Dadurch sind Millionen Menschen weiterhin Klimarisiken ausgesetzt, während hart erkämpfte Entwicklungserfolge gefährdet werden. Zwar wenden viele Entwicklungsländer bereits erhebliche öffentliche Mittel zur Bewältigung der Klimafolgen auf, doch bleiben diese Investitionen deutlich hinter dem notwendigen Umfang zurück und engen zugleich den finanzpolitischen Spielraum für andere Entwicklungsziele weiter ein.

Die jüngsten Mittelzuweisungen im Staatshaushalt Bangladeschs, einem der weltweit am stärksten vom Klimawandel bedrohten Länder, zeigen die Folgen des stockenden Fortschritts beim GGA auf nationaler Ebene. Laut dem nationalen Anpassungsplan von 2023 werden bis 2050 jährlich rund 8,5 Mrd. USD benötigt, um die Herausforderungen der Anpassung zu bewältigen. Der Staatshaushalt für 2026–2027 sieht jedoch nur rund 3,19 Milliarden USD für Klimaanpassung vor. Die auf 25 Ministerien verteilten Mittel fließen in Programme zur Katastrophenvorsorge, klimaresilienten Landwirtschaft, Ernährungssicherheit und für soziale Sicherung. Der Betrag mag hoch erscheinen, deckt aber weniger als die Hälfte des geschätzten jährlichen Anpassungsbedarfs und zeigt deutlich, dass inländische Ressourcen allein nicht ausreichen, um die Anpassungsziele zu erreichen.

Die Mittelzuweisung für Anpassungsmaßnahmen, die rund 4,15 % des Staatshaushalts ausmacht, stellt zwar eine Steigerung gegenüber den Vorjahren dar, verdeutlicht jedoch zugleich die haushaltspolitischen Zielkonflikte. Die öffentlichen Investitionen in den Klimaschutz bleiben begrenzt: Im Haushalt 2026–27 sind lediglich 814 Mio. USD für erneuerbare Energien, Energieeffizienz, emissionsarmen Transport und Aufforstung vorgesehen. Das liegt deutlich unter den geschätzten 1,78 Mrd. USD, die jährlich erforderlich sind, um Bangladeschs Ziele für erneuerbare Energien bis 2030 zu erreichen – darunter 553 Mio. USD an öffentlichen Investitionen –, während die derzeitige Zuweisung von 31,1 Mio. USD lediglich 2,2 % dieses Bedarfs deckt. Die unzureichende öffentliche Finanzierung bremst weiterhin den Ausbau erneuerbarer Energien, während Steuerbefreiungen für den Import fossiler Energieträger die Abhängigkeit von diesen Importen weiter festigen.

Für Länder wie Bangladesch ist eine auf Zuschüssen basierende Anpassungsfinanzierung daher unerlässlich. Ohne sie drohen die Klimaziele weitgehend Rhetorik zu bleiben. Eine anhaltende Unterfinanzierung kann die institutionellen Strukturen der Klimaanpassung schwächen und die über Jahre aufgebauten Umsetzungsbemühungen untergraben. Die Verantwortung dafür liegt jedoch nicht allein bei den nationalen Regierungen. Der Krieg in der Ukraine und zwischen den USA und dem Iran haben die Sorgen um Energiesicherheit, Inflation und wirtschaftliche Stabilität verschärft – und damit finanzielle Ressourcen sowie politische Aufmerksamkeit von Klimaschutz und Anpassung abgezogen.

Zugleich stehen viele klimavulnerable Länder vor einer doppelten Herausforderung: Sie müssen eskalierende Klimarisiken bewältigen und sich gleichzeitig in einem zunehmend unsicheren geopolitischen Umfeld behaupten. Zu der ohnehin langen Liste von Klimagefahren – darunter Meeresspiegelanstieg, Überschwemmungen, Dürren, Versalzung, Ernährungsunsicherheit, Vertreibung und der Verlust von Ökosystemen – sind inzwischen eine unsichere Energieversorgung, Lieferkettenstörungen und wirtschaftliche Schwankungen hinzugekommen.

Der mangelnde Fortschritt beim GGA auf der SB64 ist daher äußerst besorgniserregend. Klimavulnerable Länder benötigen kontinuierliche und ausreichende Finanzmittel, um Anpassungsmaßnahmen umzusetzen und ihre klimapolitischen Verpflichtungen zu erfüllen. Doch der politische und finanzielle Spielraum für Anpassung schrumpft – nicht, weil die Klimarisiken abgenommen hätten, sondern weil konkurrierende Krisen die politische Agenda auf nationaler wie internationaler Ebene zunehmend bestimmen. Die COP31 muss den Verhandlungen neuen Schwung verleihen, indem sie ein umsetzungsfähiges GGA beschließt, das messbar ist, den Finanzierungsbedarf berücksichtigt und auf die Umsetzung ausgerichtet ist. Dafür braucht es gemeinsame Anpassungsindikatoren, klare Rechenschaftsmechanismen und verlässliche Zuschüsse, damit besonders gefährdete Länder ihre Anpassungsprioritäten umsetzen können.

A B M Hasanuzzaman ist Fellow des Internationalen Klimaschutzstipendiums der Alexander von Humboldt-Stiftung 2025 und Gastwissenschaftler am IDOS.

Dr. Aparajita Banerjee ist Soziologin und wissenschaftliche Mitarbeiterin in der Abteilung „Umwelt-Governance“ des German Institute of Development and Sustainability (IDOS).

Categories: Diplomacy & Defense Think Tank News, Swiss News

Folgen der stockenden Verhandlungen zum globalen Anpassungsziel für Entwicklungsländer

Bonn, 6. Juli 2026. Gemeinschaften in besonders stark vom Klimawandel betroffenen Ländern passen sich an dessen Auswirkungen an, doch die nötigen Ressourcen bleiben aus.

Die alljährlichen Zwischenverhandlungen der UN-Klimarahmenkonvention im Juni (SB64) erreichten bei mehreren zentralen Agendapunkten, darunter dem Globalen Anpassungsziel (Global Goal on Adaptation, GGA), nur begrenzte Fortschritte. Das GGA ist eine Verpflichtung aller Unterzeichnerländer des Pariser Abkommens. Es soll die Anpassungsbemühungen koordinieren, Rechenschaftspflichten stärken und Finanzmittel für vulnerable Länder mobilisieren. Obwohl die Staaten den Umsetzungsrahmen finalisieren sollten, bleiben langjährige politische Streitfragen ungelöst. Entwicklungsländer kritisierten die Industrieländer, weil die schriftliche Einigung auf mindestens eine Verdreifachung der Anpassungsfinanzierung ausblieb, wie sie im „Mutirão“ der COP30 verankert ist. Ohne diese Einigung zur Finanzierung stocken die Verhandlungen.

Die festgefahrene Situation reicht über die Verhandlungsräume in Bonn hinaus. Für klimavulnerable Länder wächst mit der Lücke der Anpassungsfinanzierung die Kluft zwischen Klimaverpflichtungen und ihrer Umsetzung. Oft reichen nationale Anpassungsbudgets nicht aus und konkurrieren mit anderen dringlichen Entwicklungsprioritäten. Dadurch sind Millionen Menschen weiterhin Klimarisiken ausgesetzt, während hart erkämpfte Entwicklungserfolge gefährdet werden. Zwar wenden viele Entwicklungsländer bereits erhebliche öffentliche Mittel zur Bewältigung der Klimafolgen auf, doch bleiben diese Investitionen deutlich hinter dem notwendigen Umfang zurück und engen zugleich den finanzpolitischen Spielraum für andere Entwicklungsziele weiter ein.

Die jüngsten Mittelzuweisungen im Staatshaushalt Bangladeschs, einem der weltweit am stärksten vom Klimawandel bedrohten Länder, zeigen die Folgen des stockenden Fortschritts beim GGA auf nationaler Ebene. Laut dem nationalen Anpassungsplan von 2023 werden bis 2050 jährlich rund 8,5 Mrd. USD benötigt, um die Herausforderungen der Anpassung zu bewältigen. Der Staatshaushalt für 2026–2027 sieht jedoch nur rund 3,19 Milliarden USD für Klimaanpassung vor. Die auf 25 Ministerien verteilten Mittel fließen in Programme zur Katastrophenvorsorge, klimaresilienten Landwirtschaft, Ernährungssicherheit und für soziale Sicherung. Der Betrag mag hoch erscheinen, deckt aber weniger als die Hälfte des geschätzten jährlichen Anpassungsbedarfs und zeigt deutlich, dass inländische Ressourcen allein nicht ausreichen, um die Anpassungsziele zu erreichen.

Die Mittelzuweisung für Anpassungsmaßnahmen, die rund 4,15 % des Staatshaushalts ausmacht, stellt zwar eine Steigerung gegenüber den Vorjahren dar, verdeutlicht jedoch zugleich die haushaltspolitischen Zielkonflikte. Die öffentlichen Investitionen in den Klimaschutz bleiben begrenzt: Im Haushalt 2026–27 sind lediglich 814 Mio. USD für erneuerbare Energien, Energieeffizienz, emissionsarmen Transport und Aufforstung vorgesehen. Das liegt deutlich unter den geschätzten 1,78 Mrd. USD, die jährlich erforderlich sind, um Bangladeschs Ziele für erneuerbare Energien bis 2030 zu erreichen – darunter 553 Mio. USD an öffentlichen Investitionen –, während die derzeitige Zuweisung von 31,1 Mio. USD lediglich 2,2 % dieses Bedarfs deckt. Die unzureichende öffentliche Finanzierung bremst weiterhin den Ausbau erneuerbarer Energien, während Steuerbefreiungen für den Import fossiler Energieträger die Abhängigkeit von diesen Importen weiter festigen.

Für Länder wie Bangladesch ist eine auf Zuschüssen basierende Anpassungsfinanzierung daher unerlässlich. Ohne sie drohen die Klimaziele weitgehend Rhetorik zu bleiben. Eine anhaltende Unterfinanzierung kann die institutionellen Strukturen der Klimaanpassung schwächen und die über Jahre aufgebauten Umsetzungsbemühungen untergraben. Die Verantwortung dafür liegt jedoch nicht allein bei den nationalen Regierungen. Der Krieg in der Ukraine und zwischen den USA und dem Iran haben die Sorgen um Energiesicherheit, Inflation und wirtschaftliche Stabilität verschärft – und damit finanzielle Ressourcen sowie politische Aufmerksamkeit von Klimaschutz und Anpassung abgezogen.

Zugleich stehen viele klimavulnerable Länder vor einer doppelten Herausforderung: Sie müssen eskalierende Klimarisiken bewältigen und sich gleichzeitig in einem zunehmend unsicheren geopolitischen Umfeld behaupten. Zu der ohnehin langen Liste von Klimagefahren – darunter Meeresspiegelanstieg, Überschwemmungen, Dürren, Versalzung, Ernährungsunsicherheit, Vertreibung und der Verlust von Ökosystemen – sind inzwischen eine unsichere Energieversorgung, Lieferkettenstörungen und wirtschaftliche Schwankungen hinzugekommen.

Der mangelnde Fortschritt beim GGA auf der SB64 ist daher äußerst besorgniserregend. Klimavulnerable Länder benötigen kontinuierliche und ausreichende Finanzmittel, um Anpassungsmaßnahmen umzusetzen und ihre klimapolitischen Verpflichtungen zu erfüllen. Doch der politische und finanzielle Spielraum für Anpassung schrumpft – nicht, weil die Klimarisiken abgenommen hätten, sondern weil konkurrierende Krisen die politische Agenda auf nationaler wie internationaler Ebene zunehmend bestimmen. Die COP31 muss den Verhandlungen neuen Schwung verleihen, indem sie ein umsetzungsfähiges GGA beschließt, das messbar ist, den Finanzierungsbedarf berücksichtigt und auf die Umsetzung ausgerichtet ist. Dafür braucht es gemeinsame Anpassungsindikatoren, klare Rechenschaftsmechanismen und verlässliche Zuschüsse, damit besonders gefährdete Länder ihre Anpassungsprioritäten umsetzen können.

A B M Hasanuzzaman ist Fellow des Internationalen Klimaschutzstipendiums der Alexander von Humboldt-Stiftung 2025 und Gastwissenschaftler am IDOS.

Dr. Aparajita Banerjee ist Soziologin und wissenschaftliche Mitarbeiterin in der Abteilung „Umwelt-Governance“ des German Institute of Development and Sustainability (IDOS).

Categories: Diplomacy & Defense Think Tank News, Swiss News

Folgen der stockenden Verhandlungen zum globalen Anpassungsziel für Entwicklungsländer

Bonn, 6. Juli 2026. Gemeinschaften in besonders stark vom Klimawandel betroffenen Ländern passen sich an dessen Auswirkungen an, doch die nötigen Ressourcen bleiben aus.

Die alljährlichen Zwischenverhandlungen der UN-Klimarahmenkonvention im Juni (SB64) erreichten bei mehreren zentralen Agendapunkten, darunter dem Globalen Anpassungsziel (Global Goal on Adaptation, GGA), nur begrenzte Fortschritte. Das GGA ist eine Verpflichtung aller Unterzeichnerländer des Pariser Abkommens. Es soll die Anpassungsbemühungen koordinieren, Rechenschaftspflichten stärken und Finanzmittel für vulnerable Länder mobilisieren. Obwohl die Staaten den Umsetzungsrahmen finalisieren sollten, bleiben langjährige politische Streitfragen ungelöst. Entwicklungsländer kritisierten die Industrieländer, weil die schriftliche Einigung auf mindestens eine Verdreifachung der Anpassungsfinanzierung ausblieb, wie sie im „Mutirão“ der COP30 verankert ist. Ohne diese Einigung zur Finanzierung stocken die Verhandlungen.

Die festgefahrene Situation reicht über die Verhandlungsräume in Bonn hinaus. Für klimavulnerable Länder wächst mit der Lücke der Anpassungsfinanzierung die Kluft zwischen Klimaverpflichtungen und ihrer Umsetzung. Oft reichen nationale Anpassungsbudgets nicht aus und konkurrieren mit anderen dringlichen Entwicklungsprioritäten. Dadurch sind Millionen Menschen weiterhin Klimarisiken ausgesetzt, während hart erkämpfte Entwicklungserfolge gefährdet werden. Zwar wenden viele Entwicklungsländer bereits erhebliche öffentliche Mittel zur Bewältigung der Klimafolgen auf, doch bleiben diese Investitionen deutlich hinter dem notwendigen Umfang zurück und engen zugleich den finanzpolitischen Spielraum für andere Entwicklungsziele weiter ein.

Die jüngsten Mittelzuweisungen im Staatshaushalt Bangladeschs, einem der weltweit am stärksten vom Klimawandel bedrohten Länder, zeigen die Folgen des stockenden Fortschritts beim GGA auf nationaler Ebene. Laut dem nationalen Anpassungsplan von 2023 werden bis 2050 jährlich rund 8,5 Mrd. USD benötigt, um die Herausforderungen der Anpassung zu bewältigen. Der Staatshaushalt für 2026–2027 sieht jedoch nur rund 3,19 Milliarden USD für Klimaanpassung vor. Die auf 25 Ministerien verteilten Mittel fließen in Programme zur Katastrophenvorsorge, klimaresilienten Landwirtschaft, Ernährungssicherheit und für soziale Sicherung. Der Betrag mag hoch erscheinen, deckt aber weniger als die Hälfte des geschätzten jährlichen Anpassungsbedarfs und zeigt deutlich, dass inländische Ressourcen allein nicht ausreichen, um die Anpassungsziele zu erreichen.

Die Mittelzuweisung für Anpassungsmaßnahmen, die rund 4,15 % des Staatshaushalts ausmacht, stellt zwar eine Steigerung gegenüber den Vorjahren dar, verdeutlicht jedoch zugleich die haushaltspolitischen Zielkonflikte. Die öffentlichen Investitionen in den Klimaschutz bleiben begrenzt: Im Haushalt 2026–27 sind lediglich 814 Mio. USD für erneuerbare Energien, Energieeffizienz, emissionsarmen Transport und Aufforstung vorgesehen. Das liegt deutlich unter den geschätzten 1,78 Mrd. USD, die jährlich erforderlich sind, um Bangladeschs Ziele für erneuerbare Energien bis 2030 zu erreichen – darunter 553 Mio. USD an öffentlichen Investitionen –, während die derzeitige Zuweisung von 31,1 Mio. USD lediglich 2,2 % dieses Bedarfs deckt. Die unzureichende öffentliche Finanzierung bremst weiterhin den Ausbau erneuerbarer Energien, während Steuerbefreiungen für den Import fossiler Energieträger die Abhängigkeit von diesen Importen weiter festigen.

Für Länder wie Bangladesch ist eine auf Zuschüssen basierende Anpassungsfinanzierung daher unerlässlich. Ohne sie drohen die Klimaziele weitgehend Rhetorik zu bleiben. Eine anhaltende Unterfinanzierung kann die institutionellen Strukturen der Klimaanpassung schwächen und die über Jahre aufgebauten Umsetzungsbemühungen untergraben. Die Verantwortung dafür liegt jedoch nicht allein bei den nationalen Regierungen. Der Krieg in der Ukraine und zwischen den USA und dem Iran haben die Sorgen um Energiesicherheit, Inflation und wirtschaftliche Stabilität verschärft – und damit finanzielle Ressourcen sowie politische Aufmerksamkeit von Klimaschutz und Anpassung abgezogen.

Zugleich stehen viele klimavulnerable Länder vor einer doppelten Herausforderung: Sie müssen eskalierende Klimarisiken bewältigen und sich gleichzeitig in einem zunehmend unsicheren geopolitischen Umfeld behaupten. Zu der ohnehin langen Liste von Klimagefahren – darunter Meeresspiegelanstieg, Überschwemmungen, Dürren, Versalzung, Ernährungsunsicherheit, Vertreibung und der Verlust von Ökosystemen – sind inzwischen eine unsichere Energieversorgung, Lieferkettenstörungen und wirtschaftliche Schwankungen hinzugekommen.

Der mangelnde Fortschritt beim GGA auf der SB64 ist daher äußerst besorgniserregend. Klimavulnerable Länder benötigen kontinuierliche und ausreichende Finanzmittel, um Anpassungsmaßnahmen umzusetzen und ihre klimapolitischen Verpflichtungen zu erfüllen. Doch der politische und finanzielle Spielraum für Anpassung schrumpft – nicht, weil die Klimarisiken abgenommen hätten, sondern weil konkurrierende Krisen die politische Agenda auf nationaler wie internationaler Ebene zunehmend bestimmen. Die COP31 muss den Verhandlungen neuen Schwung verleihen, indem sie ein umsetzungsfähiges GGA beschließt, das messbar ist, den Finanzierungsbedarf berücksichtigt und auf die Umsetzung ausgerichtet ist. Dafür braucht es gemeinsame Anpassungsindikatoren, klare Rechenschaftsmechanismen und verlässliche Zuschüsse, damit besonders gefährdete Länder ihre Anpassungsprioritäten umsetzen können.

A B M Hasanuzzaman ist Fellow des Internationalen Klimaschutzstipendiums der Alexander von Humboldt-Stiftung 2025 und Gastwissenschaftler am IDOS.

Dr. Aparajita Banerjee ist Soziologin und wissenschaftliche Mitarbeiterin in der Abteilung „Umwelt-Governance“ des German Institute of Development and Sustainability (IDOS).

Categories: Diplomacy & Defense Think Tank News, Swiss News

Beyond Fragmentation: Legal Instruments, Capital Markets and the Governance of the EU Single Market

This Policy Paper examines the renewed debate on completing the EU Single Market. It argues that the challenge is not simply to adopt more EU legislation or to choose between regulations and directives, but to turn formal market access into operational market integration. Focusing on capital markets, services and governance, the paper shows that fragmentation persists when legal convergence is not matched by implementation capacity, supervisory alignment and political incentives for compliance. Completing the Single Market means making Europe the natural scale for firms, capital and innovation.

Read here in pdf the Policy Paper by Dr Apostolos Samaras, Research Fellow, European Programme ‘Ariane Condellis’, Hellenic Foundation for European and Foreign Policy (ELIAMEP).

Introduction: From Single Market Completion to European Scale“All those who, in trying to meet the economic challenges set out by the treaty of Rome, neglected the political dimension have failed. As long as [those] challenges will be addressed exclusively in an economic perspective, disregarding their political angle, we will run – I am afraid – into repeated failures”

Paul-Henri Spaak, Discours à la Chambre des Représentants, 14 June 1961.

To date the Single Market is the EU’s most significant economic achievement. However, its relevance depends on its ability to support European competitiveness under rapidly changing global conditions. In January 2025, the European Commission unveiled the so-called “competitiveness compass”, a fresh strategy aimed at revitalising EU’s dynamism (European Commission, 2025a). The Commission views competitiveness as a multifaceted concept, structured around several crucial elements including the functioning of the Single Market, access to capital, innovation, skills and infrastructure (European Commission, 2024). Within this framework, a well-functioning internal market is presented as a central condition for enabling businesses to scale, facilitating investment and supporting productivity growth across the EU.

The European Commission has consistently identified hurdles affecting the functioning of the Single Market, particularly in services and areas requiring administrative coordination (European Commission, 2020a). The aforementioned barriers increase costs for businesses, reduce legal certainty and discourage cross-border activity. Moreover, recent policy reports place these issues in a broader economic context. Draghi (2024) links Europe’s investment gap to structural inefficiencies, including fragmentation within the Single Market. Letta (2024) similarly argues that the Single Market must evolve to support scale, speed and strategic resilience. Institutional policy analysis reinforces this assessment, e.g. the International Monetary Fund (IMF) notes that Europe’s growth potential is restrained by weak productivity and limited scale (IMF, 2024).

The European Council has endorsed a renewed focus on the Single Market as a key driver of competitiveness, emphasising the need to remove barriers and improve its functioning.

These findings are indicated in current EU political priorities. The European Council has endorsed a renewed focus on the Single Market as a key driver of competitiveness, emphasising the need to remove barriers and improve its functioning (European Council, 2026). Market fragmentation is affecting investment decisions, innovation, productivity growth and the global position of European businesses, also having broader strategic implications. As recent policy analysis emphasises, the absence of an integrated internal market limits businesses’ ability to scale and raises capital costs, weakening Europe’s position in an increasingly bloc-based global economy, where size and coordination determine competitiveness (Jacques Delors Institute, 2026).

This paper argues that the next phase of Single Market reform should not be framed simply as a choice between more or less EU legislation. The central question is whether EU legal instruments, enforcement mechanisms and supervisory structures can convert formal market access into operational market integration. Capital markets and services show that fragmentation persists where legal convergence is not matched by administrative capacity, supervisory alignment and political incentives for compliance.

The Problem: What Kind of Fragmentation?Α precise understanding of fragmentation requires distinguishing between its main sources. Two factors are particularly relevant. The first is incomplete regulatory convergence. […] The second is implementation failure. Even where appropriate EU legislation exists, its application may still be uneven.

A precise understanding of fragmentation requires distinguishing between its main sources. Two factors are particularly relevant. The first is incomplete regulatory convergence. In certain areas, EU legislation does not fully eliminate cross-border burdens. Capital markets provide a clear example, where differences in insolvency law, taxation in cross-border investing and market infrastructure continue to create barriers to integration. The second is implementation failure. Even where appropriate EU legislation exists, its application may still be uneven. Although not confined to Single Market law, the persistence of infringement litigation before the Court of Justice of the European Union (CJEU) confirms that uneven application remains a structural problem in EU law enforcement, with 200 infringement actions brought between 2021 and 2025 (Court of Justice of the European Union, 2026). Enforcement mechanisms are often slow and reactive. The Commission has acknowledged the need to strengthen enforcement as part of its broader strategy (European Commission, 2022).

At a deeper level, fragmentation signifies a structural trade-off. Greater market integration entails constraints on national regulatory autonomy, especially in areas such as finance, taxation or supervision.

Moreover, Member States apply EU law within national systems shaped by domestic institutional structures and policy priorities. This can create incentives to preserve regulatory discretion or to delay reforms, particularly in politically sensitive areas, even where legal obligations are clear. At a deeper level, fragmentation signifies a structural trade-off. Greater market integration entails constraints on national regulatory autonomy, especially in areas such as finance, taxation or supervision. The extent to which this trade-off is genuinely accepted varies across Member States and over time, shaping the pace and the depth of integration.

These factors can be interlinked in practice. Regulatory divergence may endure because implementation is weak, whilst domestic political incentives sometimes discourage convergence. The European Commission’s May 2025 Single Market Strategy identifies the “Terrible Ten” barriers disrupting the market, such as restrictive national services rules, long delays in standard-setting and overly complex EU rules (European Commission, 2025b). Evidence from the services sector exemplifies this dynamic. Despite existing EU legislation, barriers remain widespread, reflecting both regulatory and implementation challenges (European Commission, 2020a).

The Digital Single Market provides a useful illustration of this broader pattern. Recent analysis identifies mutually reinforcing bottlenecks: uneven regulatory implementation, nationally siloed infrastructure, barriers to data flows and skills mobility, and insufficient growth-stage finance. This confirms that Single Market reform cannot rely on legal harmonisation alone. Uniform rules must be connected to enforcement capacity, digital infrastructure, public procurement, capital market depth and practical compliance tools if firms are to scale across borders (Aarnio et al., 2026).

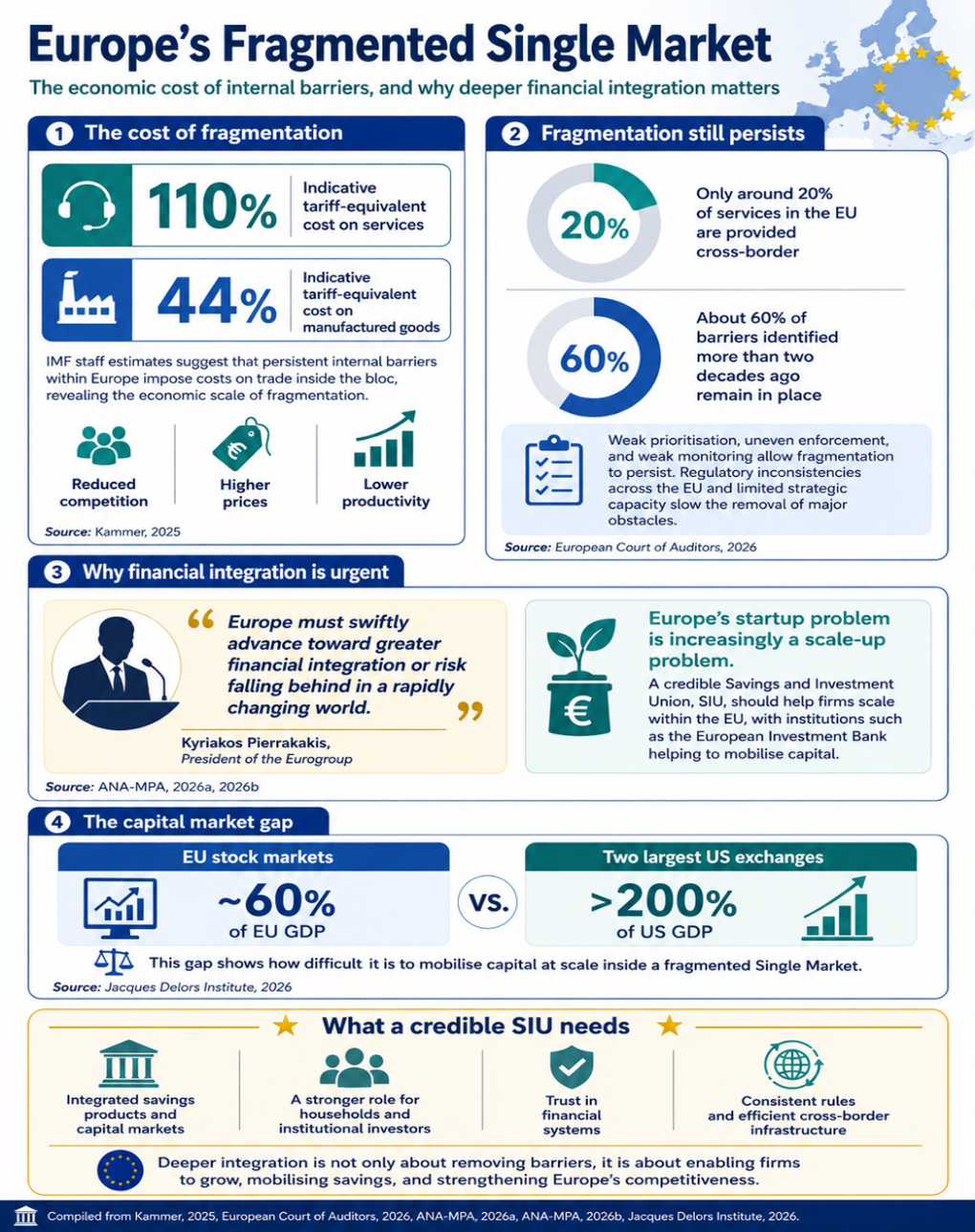

IMF staff estimates suggest that persisting internal barriers within Europe may be equivalent to an indicative 110% tariff on services and 44% for manufactured goods […] recent audit evidence finds that only around 20% of services in the EU are provided cross-border, while approximately 60% of barriers identified more than two decades ago remain in place.

IMF staff estimates suggest that persisting internal barriers within Europe may be equivalent to an indicative 110% tariff on services and 44% for manufactured goods (Kammer, 2025). This shows the economic scale of fragmentation. European consumers and businesses face these costs through reduced competition, increased prices and lower productivity. Moreover, recent audit evidence finds that only around 20% of services in the EU are provided cross-border, while approximately 60% of barriers identified more than two decades ago remain in place (European Court of Auditors, 2026). At the same time, weaknesses in prioritisation, enforcement and monitoring suggest that fragmentation persists due to regulatory inconsistencies across the bloc and limited EU strategic capacity to remove the most significant obstacles (European Court of Auditors, 2026).

A competitiveness agenda that creates startups but fails to support scaleups would leave Europe’s structural scale problem unresolved.

Kyriakos Pierrakakis, the President of the Eurogroup, has stressed that Europe faces a pivotal decision: it must swiftly advance toward greater financial integration or face the risk of falling behind in a world that is rapidly changing (ANA-MPA, 2026a). More specifically, Europe’s startup problem is increasingly a scaleup problem. Eurobarometer evidence supports the view that the Single Market should be judged not only by market access, but by its capacity to help firms grow across borders. A competitiveness agenda that creates startups but fails to support scaleups would leave Europe’s structural scale problem unresolved (European Commission, 2025c). EU innovative startups and scaleups continue to face fragmented regulatory regimes, high compliance costs, limited access to late-stage capital, skills shortages and difficulties in using cross-border procurement and institutional markets (Thomadakis & Marcus, 2025).

…EU stock markets have a combined capitalisation of roughly 60% of EU GDP, while the two largest US exchanges alone exceed 200% of US GDP

A credible SIU should therefore be judged by whether it enables firms to scale inside the EU, with institutions such as the European Investment Bank helping to mobilise capital (ANA-MPA, 2026b). It is noteworthy that EU stock markets have a combined capitalisation of roughly 60% of EU GDP, while the two largest US exchanges alone exceed 200% of US GDP (Jacques Delors Institute, 2026). This disparity highlights the structural difficulty of mobilising capital at scale within a fragmented Single Market. The SIU framing places greater emphasis on the role of households and institutional investors, as well as on the integration of savings products and capital markets. Nonetheless, mobilising savings depends on trust in financial systems, consistent regulatory frameworks and efficient cross-border infrastructure.

{kind=link}

FIGURE 1: Market barriers and the rationale for the SIU

Legal Integration and its Limits

The EU’s legislation governing the Single Market is prima facie comprehensive. It encompasses primary law provisions, specified and complemented by extensive secondary law. This common binding framework establishes directly enforceable rights for economic actors and prohibits a wide array of restrictions on cross-border activities. In that respect, EU law is sound and unavoidable.

Even though it has been established that EU legislation prohibits unjustified restrictions on the free movement of capital, services, goods, and persons, it certainly does not eliminate the conditions under which those restrictions arise.

However, the strength of EU law should not obscure its limits. Even though it has been established that EU legislation prohibits unjustified restrictions on the free movement of capital, services, goods, and persons, it certainly does not eliminate the conditions under which those restrictions arise. Nor does it ensure convergence in administrative practices, regulatory approaches or institutional capacity. These are structural limitations, since the implementation of EU law depends on national authorities that operate within different legal traditions, administrative systems and policy priorities. This leads to the familiar paradox that the same EU legal rule may produce different outcomes across Member States.

…there is increasing support for regulations (Wax & Ionta, 2026), which are binding and directly applicable, reducing the scope for divergence.

Policy debates have focused on this issue, which is also intrinsically correlated to national sovereignty concerns. Directives, as binding legal acts that allow flexibility in national transposition, granting Member States some national discretion to decide how to achieve the set objectives, have often resulted in divergent implementation. In response, there is increasing support for regulations (Wax & Ionta, 2026), which are binding and directly applicable, reducing the scope for divergence. The shift towards regulations is already visible in EU legislative practice: in recent years regulations have become the dominant instrument among legislative acts adopted under the ordinary legislative procedure (Publications Office of the European Union, n.d.). This approach aims to address possible legal confusion among Member States, without being a panacea for every problem, since ultimately all EU rules depend on national enforcement. Legal uniformity, in that sense, mitigates one aspect of market fragmentation, whilst not addressing other disparities in administrative capacity or supervisory practices.

Recent OECD evidence links regulatory compliance costs to weaker productivity and lower business dynamism.

Recent OECD evidence links regulatory compliance costs to weaker productivity and lower business dynamism (Andrews et al., 2026). This matters for the Single Market because firms experience EU law also as compliance tasks, administrative procedures and enforcement practices. Regulations can reduce one important source of fragmentation by limiting divergent national transposition, but they do not remove the practical costs of compliance. Evidence on cumulative compliance costs for SMEs shows that burdens often arise from national interpretation, monitoring and enforcement practices, as well as from the accumulation of obligations over time (European Commission, 2015). These costs may affect firms’ decisions to innovate, enter new markets or expand across borders. The implication is that the choice of legal instrument matters, but it must be accompanied by clear implementation planning, proportionate enforcement and attention to administrative capacity. Otherwise, directly applicable rules may still produce uneven market effects across Member States (European Commission, 2015; Capuano, 2025).

The increasing reliance on regulations should be treated as a governance choice, not as a shortcut to integration.

Even where EU rules are directly binding, Member States remain central to how their effects materialise for businesses and citizens (OECD, 2025). The increasing reliance on regulations should be treated as a governance choice, not as a shortcut to integration. Regulations can limit national divergence, but where they postpone application, rely heavily on implementing acts, or require substantial national administrative adjustment, they may reproduce some of the same practical problems usually associated with directives (Capuano, 2025). The question is therefore not whether regulations are preferable in abstract terms, but under what conditions they can produce uniform market effects without increasing legal complexity or weakening accountability.

Policy discussions have also explored the use of optional EU-wide legal regimes, such as the so-called “28th regime” corporate legal framework, as a means of reducing fragmentation without requiring full harmonization.

Policy discussions have also explored the use of optional EU-wide legal regimes, such as the so-called “28th regime” corporate legal framework, as a means of reducing fragmentation without requiring full harmonization (Hallak, 2026). It would allow businesses to operate under a single set of EU rules across Member States, bypassing divergent national frameworks. This approach is clearly manifesting an attempt to reconcile regulatory uniformity with political limitations on deeper harmonisation. It aims to be a transition towards a legal framework specifically designed to more effectively facilitate cross-border activities in Europe. It goes hand in hand with the argument that before venturing into the global market, European companies should prioritise strengthening their presence within Europe.

Capital Markets as a Stress Test: From Free Movement to SIURegarding the freedom of capital, primary EU law is particularly liberal. Article 63 of the Treaty on the Functioning of the European Union (TFEU) prohibits all restrictions on capital movements within the EU and between Member States and third countries. The CJEU has even interpreted EU law on capital and payments in a dynamic way that reinforces its role as a central pillar of market integration (Samaras, 2022). Even so, further provisions in the TFEU stipulate a number of exceptions to the principle of free movement of capital. Article 65 TFEU stipulates derogations related to taxation, prudential supervision of financial institutions, public policy and public security.

The free movement of capital is enshrined in primary EU law, but in practice it relies largely on trust in banks, institutions, and the country’s economic performance.

Sometimes the implementation of the free movement of capital lacks certainty. As an example, one might cite the experience of “capital controls” in Cyprus (2013-2015) and in Greece (2015-2019) over the past decade, as it provides a picture of the realistic limits of legal integration within the Single Market under conditions of economic turmoil and financial crisis. The free movement of capital is enshrined in primary EU law, but in practice it relies largely on trust in banks, institutions, and the country’s economic performance. When that trust is broken, exceptions become the norm.

Today, although no comparable emergency capital controls are in place in the Member States, the free movement of capital within the EU is still not fully utilised. Capital markets provide a clear test of the limits of the current integration model.

The gradual process of further liberalising the Single Market is not always linear. Naturally, the banking and financial sector’s stability has been prioritised during periods of severe crisis. Exceptional measures have been adopted in the past, in line with EU law. Consequently, the EU’s economic freedoms are not absolutely guaranteed in perpetuity, regardless of the state of the Member States’ domestic economies and the solutions offered by the EU at the time. Even the most liberal Treaty freedom operates within institutional, financial and crisis-management constraints. Today, although no comparable emergency capital controls are in place in the Member States, the free movement of capital within the EU is still not fully utilised.

Capital markets provide a clear test of the limits of the current integration model. Successive CMU initiatives have addressed several layers of capital-market integration, including prospectus rules, securitisation, long-term investment funds, company disclosure through the European Single Access Point (ESAP), trading transparency, listing rules and withholding tax procedures.[1] Yet these measures have not removed deeper structural fragmentation in supervision, insolvency law, taxation, market infrastructure and growth-stage finance.

This means that companies and investors face higher transaction costs and legal uncertainty when operating across borders. The European Commission has identified these frictions as key impediments to the effective functioning of capital markets and to the broader objective of financing growth within the EU (European Commission, 2020b). Recent analysis indicates that the main obstacle to deeper capital market integration lies in the limited centralisation of supervisory powers at EU level, with the European Securities and Markets Authority (ESMA) still lacking the authority required to ensure consistent application of rules across Member States (Gortsos, 2026).

More integrated capital markets support private risk sharing across Member States, improve the allocation of capital and enhance the resilience of the euro area to asymmetric shocks.

The European Central Bank (ECB) has also noted the macroeconomic importance of capital market integration. More integrated capital markets support private risk sharing across Member States, improve the allocation of capital and enhance the resilience of the euro area to asymmetric shocks (European Central Bank, 2024). Fragmentation reduces these benefits, it reinforces reliance on bank-based financing and constrains access to risk capital, particularly for innovative and high-growth businesses. The CMU agenda has addressed some of these issues through targeted legislative initiatives, facilitating cross-border investment and promoting supervisory convergence. Nevertheless, structural differences in national frameworks are still problematic in a cross-border context.

The initiative for a SIU, presented by the European Commission in March 2025, suggests a recalibration into a holistic approach that incorporates the entire EU financial system, attempting to mobilise European savings more effectively and to channel them into productive investment within the EU.

The initiative for a SIU, presented by the European Commission in March 2025, suggests a recalibration into a holistic approach that incorporates the entire EU financial system, attempting to mobilise European savings more effectively and to channel them into productive investment within the EU (European Commission, 2025d). It is designed to transform the foundational work of the two main CMU Action Plans (i.e. the pioneering 2015 CMU Action Plan and the 2020 CMU Action Plan), along with the parallel efforts to develop the Banking Union, into a high-impact, more inclusive and citizen-focused, financial engine. This is closely linked to concerns about the EU’s investment gap and the need to finance large-scale transitions, including digitalisation and decarbonisation (Draghi, 2024).

Towards a results-oriented EU governance approachThe governance of the Single Market is based largely on decentralised implementation.

The governance of the Single Market is based largely on decentralised implementation. Member States are responsible for applying EU law, while the European Commission -acting as the “guardian of the Treaties”- monitors compliance and initiates enforcement when required. It is unavoidable that structural challenges and disputes rise from time to time, since the application of EU law varies in practice across the 27 EU Member States. The infringement procedure against a Member State that fails to implement EU legislation remains a crucial enforcement tool. However, despite its usefulness, it addresses specific Member State breaches of EU law, not systemic patterns of violations. The Commission has framed enforcement as a strategic and preventive function, rather than merely a reactive infringement mechanism, with particular emphasis on own-initiative investigations, incorrect transposition of directives, and infringements that obstruct fundamental freedoms or the effective functioning of the Single Market (European Commission, 2022).

…the main challenge for the EU continues to be ineffective governance.

The completion of the Single Market also requires a credible delivery framework that combines, other than political commitment, a coherent legislative package and clear timelines (Jacques Delors Institute, 2026). Recent EU initiatives point towards a more targeted and measurable enforcement strategy. The “2026 Annual Single Market and Competitiveness” report introduces the first annual “Single Market Enforcement Agenda”, focused on priority barriers such as late payments and obstacles in construction and installation services linked to the green transition, while simplification packages seek to reduce administrative burdens and make Single Market rules easier to apply in practice (European Commission, 2026). Nonetheless, institutional limits hinder enforcement. Coordination mechanisms rely on cooperation and do not always generate strong incentives for compliance. Consequently, the main challenge for the EU continues to be ineffective governance.

A turning point appears to be marked by more recent developments towards a results-oriented EU governance approach. The joint “One Europe, One Market” roadmap, agreed in late April 2026 between the European Parliament, the Council and the Commission, seeks to introduce a structured implementation framework through priority legislative deliverables and clear timelines, as well as regular monitoring through quarterly stocktaking. Europe’s fragmentation was translated into a structured work programme built around five priorities: simplifying rules, deepening Single Market integration, strengthening trade, reducing energy prices while advancing decarbonisation, and driving the digital and AI transformation, supported by more than forty legislative and policy deliverables.

The roadmap shows the political commitment of the EU institutions for setting out concrete steps towards a more operational Single Market governance (Council of the European Union, 2026). It converts a broad competitiveness agenda into a delivery test: capital markets, energy, digital infrastructure and industrial policy are placed within one political framework, with timelines that make delays more visible and politically costly (Letta, 2026a).

{kind=link}

FIGURE 2: “One Europe, One Market” roadmap (April 2026), from political commitment to measurable delivery

The roadmap’s “market integration and supervision package” is particularly relevant in this respect, since the Commission’s December 2025 proposals seek to address capital-market fragmentation through changes to trading, post-trading, asset management and ESMA supervision, confirming that the SIU depends not only on new rules but on a more integrated supervisory architecture (European Commission, 2025e).

Policy RecommendationsCompleting the Single Market requires targeted action. The adoption of these strategic priorities is strongly encouraged:

- Target harmonisation and implementation where fragmentation is structural: EU legislative action should focus on areas such as insolvency, taxation procedures and other market obstacles, where national discrepancies create permanent barriers. Where the Treaty basis allows it, regulations may be more effective than directives, since they reduce transposition delays and limit divergent national implementation. Moreover, the Commission should track the implementation of major Single Market initiatives early, using detailed guidance and reporting to prevent new fragmentation from emerging. Attention should be paid to reducing “gold-plating” (adding extra layers of rules at the national level), which often increases compliance costs without clear policy justification.

- Reinforce supervisory convergence in capital markets: As has been pointed out in the Draghi Report (2024), the EU lacks a single securities market regulator. The ESMA ought to be transformed to serve as the sole common regulator for all securities markets within the EU. The EU should strengthen convergence through the ESMA, reinforcing transparency and technical standards, attaining a more unified supervision of capital markets.

- Constitutional discipline for restrictions on capital movements: Past episodes of capital controls show that EU law can accommodate emergency restrictions on capital movements where they are justified, proportionate and temporary. The unresolved issue is institutional. These safeguards have operated mainly through ad hoc assessment and monitoring, rather than through a permanent framework designed to protect capital-market integration. The EU should therefore develop, first through secondary legislation and eventually through Treaty reform, a stricter constitutional discipline for the use of Article 65 TFEU. Its provisions should not be abolished, since taxation, prudential supervision and public policy/security remain legitimate public interests. Its invocation, however, should be tied to clearer EU-level conditions: notification, time limitation, strict periodic review and consistency with the objective of capital-market integration. The aim would not be to invent new legality criteria, but to make their application more predictable, reviewable and aligned with the completion of the SIU.

Eliminating internal obstacles across the EU is essential for enabling market dynamics to operate effectively on a large scale.

In 2024, the findings and recommendations of the Letta and Draghi reports had been met with widespread enthusiasm (Kritikos, 2024). Eliminating internal obstacles across the EU is essential for enabling market dynamics to operate effectively on a large scale. A true unified market is needed, ensuring that conducting business between Vilnius and Madrid is as seamless as it is between Athens and Thessaloniki. The competitiveness debate is therefore also a debate about scale. The EU’s difficulty is that companies, banks and capital markets are primarily organised around national markets. In a global economy shaped by continental-scale competitors from the United States and China, the relevant benchmark is whether businesses in the EU can achieve sufficient growth to establish themselves as truly European entities, rather than remaining confined to national prominence. This does not alter the fact that slow convergence may be insufficient in sectors where technological cycles and global competition move faster than EU implementation.

A more integrated Single Market needs rules that are clear and sufficiently uniform to support cross-border growth, while avoiding unnecessary procedural burdens that make compliance easier for incumbents than for new entrants.

A more integrated Single Market needs rules that are clear and sufficiently uniform to support cross-border growth, while avoiding unnecessary procedural burdens that make compliance easier for incumbents than for new entrants. National regulatory discretion may protect domestic dominant players and, possibly, reduce unwanted competitive pressure from other Member States. This might explain why many barriers still exist even when their aggregate cost to the EU economy is widely recognised. Completing the Single Market requires confronting the domestic interests that benefit from partial integration.

A functioning SIU should be assessed by whether it enables European firms to grow within Europe, rather than pushing them towards capital markets elsewhere.

Greater scale should not be understood as a goal only for large Member States or large firms. Smaller Member States and SMEs may benefit most from a genuinely integrated Single Market, because domestic scale is structurally limited. Deeper integration can expand their addressable market and create more credible paths from local innovation to European growth. Besides, Europe does not lack startups or entrepreneurial talent, but many firms face a financing and market-size ceiling once they move from creation to scaleup. A functioning SIU should be assessed by whether it enables European firms to grow within Europe, rather than pushing them towards capital markets elsewhere.

Recent EU policy developments set out the way forward regarding greater regulatory uniformity and less economic overreliance on third countries. This direction addresses important aspects of the problem. However, legal convergence does not automatically produce effective integration. The central challenge is mostly operational, since the EU has demonstrated its ability to identify barriers and design policy responses. Ensuring consistent implementation across Member States is more difficult. The long-term political sustainability of the Single Market depends also on ensuring that mobility remains a choice rather than an obligation. As emphasised in recent policy debates, deeper integration must be accompanied by economic and social cohesion in order to remain politically viable (Letta, 2026b).

Completing the Single Market should be understood not only as an economic reform, but as a condition for European resilience and sovereignty.

The link between competitiveness and European security is also central to the Single Market debate. In a global economy, fragmentation weakens the EU’s capacity to invest, innovate and act strategically. Completing the Single Market should be understood not only as an economic reform, but as a condition for European resilience and sovereignty (Letta & Lamy, 2026). It is time for the EU to compete with the dominant players, benefitting from a higher degree of autonomy by boosting its economy. For the EU this requires a decisive shift from agenda-setting to delivery. It implies departing from mediocrity, with stronger enforcement, greater administrative capacity and sustained political commitment.

Completing the Single Market means making Europe the natural scale of economic activity, rather than leaving firms, capital and innovation trapped in national markets.

From the early stages of the internal market, European policymakers recognised that incomplete integration risks reducing the market to a form of managed openness instead of a fully functioning economic space (European Commission, 1985). The struggle over the same strategic choice is still relevant today. The key question is whether Europe can transition from a culture of national protectionism to a European-scale mindset. Completing the Single Market means making Europe the natural scale of economic activity, rather than leaving firms, capital and innovation trapped in national markets.

ReferencesAarnio, R., Bogucki, A., Jorge Ricart, R., Timmers, P., & Vainio, T. (2026). Building One Europe, One Market: Four strategic priorities for the digital single market (Sitra Studies 258). Sitra.

ANA-MPA. (2026a, March 17). Pierrakakis at Euronext: SIU will boost job quality across Europe. https://www.amna.gr/mobile/article/978705/Pierrakakis-at-Euronext-SIU-will-boost-job-quality-across-Europe

ANA-MPA. (2026b, May 13). Pierrakakis: We need greater integration in Europe, bank mergers, larger businesses. https://www.amna.gr/article/992554/pierrakakis-we-need-greater-integration-in-europe–bank-mergers–larger-businesses

Andrews, D., Turban, S., & Tyros, S. (2026). Regulatory compliance costs and productivity: New task-based evidence (OECD Economics Department Working Papers No. 1856). OECD Publishing. https://doi.org/10.1787/1c1da52e-en

Capuano, V. (2025). New legislative approach with old legislative tools: The recent (ab)use of regulations in European Union law. Eurojus, 4, 145–163. https://rivista.eurojus.it/new-legislative-approach-with-old-legislative-tools-the-recent-abuse-of-regulations-in-european-union-law/

Council of the European Union. (2026). One Europe, One Market Roadmap of the European Parliament, the Council of the European Union and the European Commission (ST-8473/26).

https://data.consilium.europa.eu/doc/document/ST-8473-2026-INIT/en/pdf

Court of Justice of the European Union. (2026). Annual report 2025: Statistics concerning the judicial activity of the Court of Justice. https://curia.europa.eu/site/upload/docs/application/pdf/2026-05/ra_en_court_statistiques_25.pdf

Draghi, M. (2024). The future of European competitiveness. European Commission. Part A: https://commission.europa.eu/document/download/97e481fd-2dc3-412d-be4c-f152a8232961_en; Part B: https://commission.europa.eu/document/download/ec1409c1-d4b4-4882-8bdd-3519f86bbb92_en?filename=The%20future%20of%20European%20competitiveness_%20In-depth%20analysis%20and%20recommendations_0.pdf

European Central Bank. (2024). Financial integration and structure in the euro area. https://www.ecb.europa.eu/press/fie/html/ecb.fie202406~c4ca413e65.en.html

European Commission. (1985). Completing the internal market: White paper from the Commission to the European Council (Milan, 28–29 June 1985) (COM(85) 310 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:51985DC0310

European Commission [Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs & Centre for Strategy & Evaluation Services]. (2015). Cost of the cumulative effects of compliance with EU law for SMEs: final report. Publications Office. https://data.europa.eu/doi/10.2873/554243

European Commission. (2020a). Identifying and addressing barriers to the Single Market (COM(2020) 93 final).

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0093

European Commission. (2020b). A Capital Markets Union for people and businesses: New action plan (COM(2020) 590 final).

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0590

European Commission. (2022). Enforcing EU law for a Europe that delivers (COM(2022) 518 final).

https://commission.europa.eu/publications/communication-commission-enforcing-eu-law-europe-delivers_en

European Commission. (2024). The 2024 Annual Single Market and Competitiveness Report (COM(2024) 77 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52024DC0077

European Commission. (2025a). A Competitiveness Compass for the EU (COM(2025) 30 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52025DC0030

European Commission. (2025b). The Single Market: Our European home market in an uncertain world (COM(2025) 500 final). https://single-market-economy.ec.europa.eu/publications/single-market-our-european-home-market-uncertain-world_en

European Commission. (2025c). Startups, scaleups and entrepreneurship. [Flash Eurobarometer 559]. https://europa.eu/eurobarometer/surveys/detail/3359

European Commission. (2025d). Savings and Investments Union: A strategy to foster citizens’ wealth and economic competitiveness in the EU (COM(2025) 124 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52025DC0124

European Commission. (2025e). Market integration and supervision package. https://finance.ec.europa.eu/publications/market-integration-and-supervision-package_en

European Commission. (2026). The 2026 Annual Single Market and Competitiveness Report (COM(2026) 46 final).

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2026:46:FIN

European Council. (2026). European Council conclusions, 19 March 2026.

https://www.consilium.europa.eu/en/meetings/european-council/2026/03/19/

European Court of Auditors. (2026). Single market for services: Commission action to remove barriers to cross-border services still insufficient (Special Report No 13/2026). https://www.eca.europa.eu/en/publications/SR-2026-13

Gortsos, C. (2026). European (EU) capital markets law at (close to) 50: Historical evolution and missing elements (EBI Working Paper No. 207). European Banking Institute. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6689178

Hallak, I. (2026, April). The 28th regime corporate legal framework (PE 785.710). European Parliamentary Research Service, European Parliament. https://www.europarl.europa.eu/thinktank/en/document/EPRS_BRI(2026)785710

IMF. (2024, October). Regional Economic Outlook for Europe: A Recovery Short of Europe’s Full Potential.

Jacques Delors Institute. (2026). One Europe, One market: Europe’s strongest response to a world in transformation. https://institutdelors.eu/content/uploads/2026/04/One-Europe-One-Market_paper_v3-1.pdf

Kammer, A. (2025, June). Europe’s integration imperative. International Monetary Fund. https://www.imf.org/en/publications/fandd/issues/2025/06/europes-integration-imperative-alfred-kammer

Kritikos, A. (2024). The Letta and Draghi reports: The only way to go, despite the hurdles (European Economy Policy Briefs No. 5/2024). Hellenic Foundation for European and Foreign Policy (ELIAMEP). https://www.eliamep.gr/wp-content/uploads/2024/11/Policy-briefs-special-edition-Leventis-5-EN-.pdf

Letta, E. (2024). Much more than a market. Council of the European Union.

https://www.consilium.europa.eu/media/ny3j24sm/much-more-than-a-market-report-by-enrico-letta.pdf

Letta, E. (2026a, May). One Europe, One Market Roadmap: Building Europe’s capacity to act. Centre for Economic Policy Research. https://cepr.org/system/files/publication-files/299775-one_europe_one_market_roadmap_building_europe_s_capacity_to_act.pdf

Letta, E. (2026b, February 26). One Europe. One market. Time to complete the EU single market. Politico. https://www.politico.eu/article/time-complete-eu-european-single-market-next-step/

Letta, E., & Lamy, P. (2026, March 17). Now more than ever, Europe must complete the Single Market. Project Syndicate. https://www.project-syndicate.org/commentary/eu-completing-single-market-key-to-defense-energy-security-tech-sovereignty-by-enrico-letta-and-pascal-lamy-2026-03

OECD. (2025). Better Regulation Practices across the European Union 2025. OECD Publishing. https://doi.org/10.1787/6f007516-en

Publications Office of the European Union. (n.d.). Legal acts – statistics. EUR-Lex. https://eur-lex.europa.eu/statistics/legislative-acts-statistics.html

Samaras, A. (2022). Οι κεφαλαιακοί περιορισμοί στο σύγχρονο ενωσιακό δίκαιο [Restrictions on the free movement of capital in contemporary EU law]. Nomiki Bibliothiki.

Thomadakis, A., & Marcus, J. S. (2025). Identification of hurdles that companies, especially innovative start-ups, face in the EU justifying the need for a 28th regime (PE 775.947). European Parliament, Policy Department for Justice, Civil Liberties and Institutional Affairs. https://www.europarl.europa.eu/RegData/etudes/STUD/2025/775947/IUST_STU(2025)775947_EN.pdf

Wax, E., & Ionta, N. (2026, April 28). Who killed the directive? Euractiv.

https://www.euractiv.com/news/rapporteur-who-killed-the-directive/

[1] See, indicatively, Regulation (EU) 2017/1129; Regulation (EU) 2017/2402; Regulation (EU) 2023/606; Regulation (EU) 2023/2859; Directive (EU) 2024/790; Regulation (EU) 2024/791; Regulation (EU) 2024/2809; Directive (EU) 2024/2811; Council Directive (EU) 2025/50.

Categories: Diplomacy & Defense Think Tank News, Swiss News

Tempo darf kein Ersatz für Demokratie sein

Die EU-Erweiterung auf dem Westbalkan ist strategisch wichtig. Doch wer den Beitrittsprozess beschleunigen will, darf Demokratie und Rechtsstaatlichkeit nicht zur Nebensache machen. Ein Beitrag von Karina Mross.

Categories: Diplomacy & Defense Think Tank News, European Union

Tempo darf kein Ersatz für Demokratie sein

Die EU-Erweiterung auf dem Westbalkan ist strategisch wichtig. Doch wer den Beitrittsprozess beschleunigen will, darf Demokratie und Rechtsstaatlichkeit nicht zur Nebensache machen. Ein Beitrag von Karina Mross.

Categories: Diplomacy & Defense Think Tank News, European Union

Tempo darf kein Ersatz für Demokratie sein

Die EU-Erweiterung auf dem Westbalkan ist strategisch wichtig. Doch wer den Beitrittsprozess beschleunigen will, darf Demokratie und Rechtsstaatlichkeit nicht zur Nebensache machen. Ein Beitrag von Karina Mross.

Categories: Diplomacy & Defense Think Tank News, European Union

The 2028-2034 Multi-Annual Financial Framework: three scenarios on the potential future of EU financing for global multilateralism

This ETTG policy brief analyses the state of play of EU funding to and cooperation with the United Nations system, before considering future possibilities and challenges in relation to the ongoing negotiations of the next Multi-Annual Financial Framework (MFF, 2028–34), notably the Global Europe Instrument. Although neither the MFF nor the Global Europe Instrument Regulation are expected to include concrete provisions on EU funding to the UN system, they frame the political priorities and define legal boundaries and criteria through which the EU will shape its programming and select its implementation partners. Through these parameters, the question is whether the new MFF will operationalise and ensure the Union’s strategic defence of multilateralism and partnership with the UN, alone and through Team Europe, or if the new rules instead result in a de-facto reduction of the EU’s political and financial support to the UN system.

Categories: Diplomacy & Defense Think Tank News, European Union

The 2028-2034 Multi-Annual Financial Framework: three scenarios on the potential future of EU financing for global multilateralism

This ETTG policy brief analyses the state of play of EU funding to and cooperation with the United Nations system, before considering future possibilities and challenges in relation to the ongoing negotiations of the next Multi-Annual Financial Framework (MFF, 2028–34), notably the Global Europe Instrument. Although neither the MFF nor the Global Europe Instrument Regulation are expected to include concrete provisions on EU funding to the UN system, they frame the political priorities and define legal boundaries and criteria through which the EU will shape its programming and select its implementation partners. Through these parameters, the question is whether the new MFF will operationalise and ensure the Union’s strategic defence of multilateralism and partnership with the UN, alone and through Team Europe, or if the new rules instead result in a de-facto reduction of the EU’s political and financial support to the UN system.

Categories: Diplomacy & Defense Think Tank News, European Union

The 2028-2034 Multi-Annual Financial Framework: three scenarios on the potential future of EU financing for global multilateralism

This ETTG policy brief analyses the state of play of EU funding to and cooperation with the United Nations system, before considering future possibilities and challenges in relation to the ongoing negotiations of the next Multi-Annual Financial Framework (MFF, 2028–34), notably the Global Europe Instrument. Although neither the MFF nor the Global Europe Instrument Regulation are expected to include concrete provisions on EU funding to the UN system, they frame the political priorities and define legal boundaries and criteria through which the EU will shape its programming and select its implementation partners. Through these parameters, the question is whether the new MFF will operationalise and ensure the Union’s strategic defence of multilateralism and partnership with the UN, alone and through Team Europe, or if the new rules instead result in a de-facto reduction of the EU’s political and financial support to the UN system.

Categories: Diplomacy & Defense Think Tank News, Europäische Union

Under negotiation: examining the development of Sámi-EU Arctic relations through the lens of norms and political legitimacy

Since 1993, the Sámi have been the only recognized Indigenous people within the European Union. However, their official engagement with European politics has been limited. This has recently begun to change, as the EU’s ongoing Arctic pivot has drawn Sámi political actors to Brussels. Using the English School approach, this case study traces the evolution of Sámi–EU relations from the early 1990s to the present to explore and analysis the mechanisms of engagement the Sámi have used to gain access to high-level European decision-making and what the EU itself should hope to gain through stronger ties with this Indigenous people. The analysis of these events reveals a growing political relationship between the Sámi and the EU. However, shifting political conditions and the absence of a formal European-level framework for Indigenous Peoples’ Rights, constrain the potential for more equitable relations both within the European sphere and Arctic.

Categories: Diplomacy & Defense Think Tank News, European Union

Under negotiation: examining the development of Sámi-EU Arctic relations through the lens of norms and political legitimacy

Since 1993, the Sámi have been the only recognized Indigenous people within the European Union. However, their official engagement with European politics has been limited. This has recently begun to change, as the EU’s ongoing Arctic pivot has drawn Sámi political actors to Brussels. Using the English School approach, this case study traces the evolution of Sámi–EU relations from the early 1990s to the present to explore and analysis the mechanisms of engagement the Sámi have used to gain access to high-level European decision-making and what the EU itself should hope to gain through stronger ties with this Indigenous people. The analysis of these events reveals a growing political relationship between the Sámi and the EU. However, shifting political conditions and the absence of a formal European-level framework for Indigenous Peoples’ Rights, constrain the potential for more equitable relations both within the European sphere and Arctic.

Categories: Diplomacy & Defense Think Tank News, European Union

Under negotiation: examining the development of Sámi-EU Arctic relations through the lens of norms and political legitimacy

Since 1993, the Sámi have been the only recognized Indigenous people within the European Union. However, their official engagement with European politics has been limited. This has recently begun to change, as the EU’s ongoing Arctic pivot has drawn Sámi political actors to Brussels. Using the English School approach, this case study traces the evolution of Sámi–EU relations from the early 1990s to the present to explore and analysis the mechanisms of engagement the Sámi have used to gain access to high-level European decision-making and what the EU itself should hope to gain through stronger ties with this Indigenous people. The analysis of these events reveals a growing political relationship between the Sámi and the EU. However, shifting political conditions and the absence of a formal European-level framework for Indigenous Peoples’ Rights, constrain the potential for more equitable relations both within the European sphere and Arctic.

Categories: Diplomacy & Defense Think Tank News, Europäische Union

How UN Peacekeeping Operations Are Adapting to Contingency Measures

The UN’s ongoing liquidity crisis has forced peacekeeping operations to implement contingency measures that have significantly reduced personnel, patrols, mission footprints, and programmatic activities. As missions adapt to these constraints, they face difficult trade-offs in maintaining mandate delivery while responding to increasingly complex security environments.

In this context, the International Peace Institute (IPI), in partnership with the permanent missions of Denmark, Germany, the Netherlands, and Pakistan to the United Nations, convened a workshop to examine how UN peacekeeping operations are adapting to contingency measures. The discussion brought together member-state representatives and UN officials from headquarters and the field to assess the operational implications of the cuts and identify lessons for the future of peacekeeping.

Key themes from the discussion included the growing reliance on mobile operational approaches, the impact of reduced mission presence on the protection of civilians and community engagement, increasing risks to peacekeeper safety and security, the opportunities and limits of digital technologies, the importance of strategic communication with host states and local communities, and the critical role of partnerships in sustaining mandate implementation amid resource constraints.

The post How UN Peacekeeping Operations Are Adapting to Contingency Measures appeared first on International Peace Institute.

Categories: Diplomacy & Defense Think Tank News, European Union

The Cyprus Presidency of the Council of the EU : An Assessment in a Time of Geopolitical Turmoil

Cleopatra Kitti, Senior Policy Advisor to ELIAMEP and Founder of the Mediterranean Growth Initiative, offers a review of Cyprus’s Presidency of the Council of the European Union, which concluded a few days ago.

Read the ELIAMEP Explainer here.

Categories: Diplomacy & Defense Think Tank News, European Union

Täter geben sich Tipps im Internet: Schlag gegen riesiges Vergewaltiger-Netzwerk in Europa

Europäischen Ermittlern ist es gelungen, ein Vergewaltiger-Netzwerk zu zerschlagen. 156 Opfer und Täter konnten identifiziert werden. Ermittlungen in neun Ländern enthüllen Tausch von Anleitungen zu Betäubungsmitteln und Missbrauch.

Categories: Diplomacy & Defense Think Tank News, Swiss News

Marcel Fratzscher: „Das Reformpaket bleibt ein Kompromiss mit sozialer Schieflage“

Die Spitzen von Union und SPD haben sich auf ein Reformpaket für wirtschaftliches Wachstum und soziale Sicherheit verständigt. Es folgt eine Einordnung von Marcel Fratzscher, Präsident des Deutschen Instituts für Wirtschaftsforschung (DIW Berlin):

Die Einigung auf das Reformpaket beendet eine lange Hängepartie in der Bundesregierung. Sein Beitrag zur Lösung der strukturellen Probleme Deutschlands dürfte jedoch begrenzt bleiben. Das Paket enthält eine Reihe von guten und sinnvollen Elementen. Vor allem der Abbau von Bürokratie, die Ziele beim Wohnungsbau und die steuerliche Entlastung bis in die Mitte hinein sind positive Aspekte. Es ist aber nicht der große Wurf, sondern eher ein Symbolpaket. Es wird der deutschen Wirtschaft nicht den gewünschten Impuls für Wachstum und Wettbewerbsfähigkeit geben. Es handelt sich um einen politischen Kompromiss mit begrenzten Ambitionen, der die großen Differenzen innerhalb der Bundesregierung zeigt und drei Botschaften enthalten soll: die Entlastung der Mitte, die Flexibilisierung für Unternehmen und eine härtere Linie beim Sozialstaat.

Zudem mangelt es in dem Vorstoß an Gerechtigkeit. Es hat eine soziale Schieflage, da der Fokus auf der Entlastung von Unternehmen liegt, zum Teil zulasten der Beschäftigten. Die Ausweitung der sachgrundlosen Befristung und die teilweise Aufweichung des Kündigungsschutzes als großen Wurf zu verkaufen, ist nicht seriös. Auch durch die geplanten Reformen bei Rente, Gesundheit und Pflege werden vor allem Menschen mit wenig Einkommen und Ersparnissen harte Einschnitte erfahren. Die Begrenzung der Westbalkan-Regelung auf 25.000 Personen pro Jahr kann den Arbeitsmarkt in Engpassbranchen zusätzlich belasten. Unter dem Strich bedeutet das Reformpaket Einschnitte vor allem für Menschen mit geringen, aber auch mit mittleren Einkommen.

Die Steuerreform ist unambitioniert, nicht ausfinanziert und entlastet zwar auch Familien und mittlere Einkommen, aber in absoluten Euro-Beträgen profitieren vor allem höhere Erwerbseinkommen unterhalb der Reichensteuer-Schwelle. Eine echte Entlastung kleiner und mittlerer Einkommen müsste stärker bei Sozialabgaben, Transfers oder Erwerbstätigenzuschüssen ansetzen - dies fehlt jedoch größtenteils. Bei der Steuerreform hat sich die Union durchgesetzt, da die Erhöhung des Reichensteuersatzes ab 250.000 Euro Jahreseinkommen eher symbolisch ist und dem Staat nur geringe zusätzliche Einnahmen verschaffen wird. Der Steuerreform fehlt Ehrlichkeit, denn es gibt faktisch keine annähernd ausreichende Gegenfinanzierung. Dass der bayerische Ministerpräsident Söder die Verhinderung einer Kürzung des Dienstwagenprivilegs als großen Erfolg verkauft, spricht für sich.

Germany's Security Council defeat: rethinking influence in a multipolar world

Germany's failure to secure a non-permanent seat on the UN Security Council is more than a diplomatic setback. It is a structural signal; and a credibility problem. For decades, Germany cultivated a reputation as an honest broker: a power that applied international law consistently. That reputation has taken damage. Germany's hesitant position toward Israel’s conduct in Gaza and Lebanon, and its evasive response to the US’ intervention in Venezuela, have seeded a perception of selectivity – that international legal norms are called for when politically convenient, and set aside when one’s own history or current dependencies make this difficult. In a world where countries from across Africa, Asia and Latin America are increasingly attentive to such inconsistencies, this matters. Credibility, once spent, is difficult to rebuild.

Germany's Security Council defeat: rethinking influence in a multipolar world

Germany's failure to secure a non-permanent seat on the UN Security Council is more than a diplomatic setback. It is a structural signal; and a credibility problem. For decades, Germany cultivated a reputation as an honest broker: a power that applied international law consistently. That reputation has taken damage. Germany's hesitant position toward Israel’s conduct in Gaza and Lebanon, and its evasive response to the US’ intervention in Venezuela, have seeded a perception of selectivity – that international legal norms are called for when politically convenient, and set aside when one’s own history or current dependencies make this difficult. In a world where countries from across Africa, Asia and Latin America are increasingly attentive to such inconsistencies, this matters. Credibility, once spent, is difficult to rebuild.

Germany's Security Council defeat: rethinking influence in a multipolar world

Germany's failure to secure a non-permanent seat on the UN Security Council is more than a diplomatic setback. It is a structural signal; and a credibility problem. For decades, Germany cultivated a reputation as an honest broker: a power that applied international law consistently. That reputation has taken damage. Germany's hesitant position toward Israel’s conduct in Gaza and Lebanon, and its evasive response to the US’ intervention in Venezuela, have seeded a perception of selectivity – that international legal norms are called for when politically convenient, and set aside when one’s own history or current dependencies make this difficult. In a world where countries from across Africa, Asia and Latin America are increasingly attentive to such inconsistencies, this matters. Credibility, once spent, is difficult to rebuild.

Pages

the old site is here

© 2012-2015 Europa Varietas Foundation © 2015-2020 Europa Varietas Association

www.europavarietas.org | info(@)europavarietas(dot)org | Switzerland

This is a GDPR ready site

We are looking for sponsors for the English translation of these books, please contact turkeandras(at)gmail(dot)com